Page 61 - Bespoke EPG 2017 Digital

P. 61

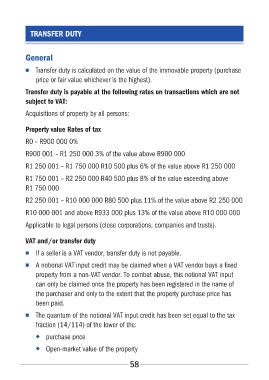

TRANSFER DUTY

General

■■ Transfer duty is calculated on the value of the immovable property (purchase

price or fair value whichever is the highest).

Transfer duty is payable at the following rates on transactions which are not

subject to VAT:

Acquisitions of property by all persons:

Property value Rates of tax

R0 – R900 000 0%

R900 001 – R1 250 000 3% of the value above R900 000

R1 250 001 – R1 750 000 R10 500 plus 6% of the value above R1 250 000

R1 750 001 – R2 250 000 R40 500 plus 8% of the value exceeding above

R1 750 000

R2 250 001 – R10 000 000 R80 500 plus 11% of the value above R2 250 000

R10 000 001 and above R933 000 plus 13% of the value above R10 000 000

Applicable to legal persons (close corporations, companies and trusts).

VAT and / or transfer duty

■■ If a seller is a VAT vendor, transfer duty is not payable.

■■ A notional VAT input credit may be claimed when a VAT vendor buys a fixed

property from a non-VAT vendor. To combat abuse, this notional VAT input

can only be claimed once the property has been registered in the name of

the purchaser and only to the extent that the property purchase price has

been paid.

■■ The quantum of the notional VAT input credit has been set equal to the tax

fraction (14 / 114) of the lower of the:

◆◆ purchase price

◆◆ Open-market value of the property

58